Securing Nonprofits with Customized Insurance

Nonprofit organizations have unique risk exposures and coverage needs compared to conventional businesses. Specialized nonprofits for insurance helps safeguard their charitable mission and limited financial resources from crippling liabilities. Tailoring policies appropriately is key.

Exposures Facing Nonprofits

Unlike commercial entities, nonprofits serve community causes rather than generating profits. But they face many key risks requiring insurance buffers, including:

– Allegations of misconduct or negligence by volunteers, staff or board members

– Injury liabilities to beneficiaries, donors or visitors at events

– Property damage to offices, vehicles or equipment from accidents or natural disasters

– Hacks or data breaches compromising sensitive information

– Financial losses or disputes impacting funding and grants

Such exposures can severely affect nonprofits if their insurance fails to meet such scenarios.

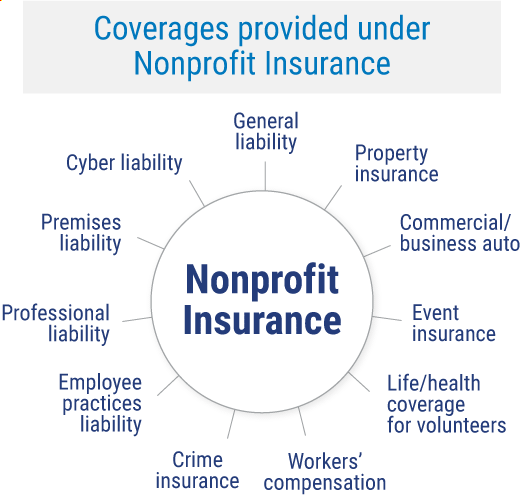

Essential Nonprofit Insurance Policies

Given their unique risks, nonprofits need tailored solutions aligning to their size, sector and local regulations. some of the most vital covers to consider are:

– Directors and Officers (D&O) liability insurance protecting board members and executives from personal legal liabilities over actual or alleged wrongful acts while managing the nonprofit. Employment practices liability insurance also falls under this.

– Commercial general liability insurance covering legal liabilities, litigation costs and settlements for third-party bodily injuries or property damage caused due to nonprofit operations. Coverage applies to premises risks, fundraising events, products, volunteers, etc.

– Professional liability insurance shielding against errors and omissions arising from a nonprofit’s professional services or advice that fail to meet standards. Common for mental health nonprofits, shelters, etc.

– Crime insurance for financial losses from theft, embezzlement, cyber fraud by own employees or third parties. Crucial given nonprofits’ vulnerability to such incidents.

– Property insurance protecting physical assets like offices, equipment, donation stock against damage perils like fires, floods. Helps avoid major disruptions.

Additionally, global nonprofits also need specialized policies like kidnap and ransom insurance for staff in high-risk regions and foreign voluntary workers coverage for overseas volunteers.

By securing financial support for adversity, purpose-built nonprofit insurance ensures continued community service despite unforeseen litigation or losses. It is an obligatory organizational expense.